How Wall Street’s ‘Fear Gauge’ Is Being Rigged, According To One Whistleblower

By Mark Decambre and Frnacine Mckenna – Market Watch.com

One of the most popular measures of volatility is being manipulated, charges one individual who submitted a letter anonymously to the Securities and Exchange Commission and the Commodity Futures Trading Commission.

The letter makes the claim to regulators that fake quotes for the S&P 500 index SPX, +1.34% are skewing levels of the Cboe Volatility Index VIX, -22.87% which reflects bearish and bullish options bets 30-days in the future on the S&P 500 to gauge implied stock-market volatility (see excerpt from the letter below).

| The flaw allows trading firms with sophisticated algorithms to move the VIX up or down by simply posting quotes on S&P options and without needing to physically engage in any trading or deploying any capital. This market manipulation has led to multiple billions in profits effectively taken away from institutional and retail investors and cashed in by unethical electronic option market makers. |

The whistleblower’s claims are consistent with those documented by John Griffin, professor of finance at the University of Texas and Ph.D. candidate Amin Shams in May 2017 in research that says the cost of manipulating less-liquid SPX options would be more than paid for by a successful bet on the direction of the VIX. The paper is consistent with the whistleblower’s conclusion—that manipulators are moving prices of the SPX options by spoofing at settlement—entering quotes for trades that are never executed—to “paint the tape” and, therefore, influence the value of expiring VIX derivatives.

The VIX has underpinned a number of strategies described as so-called short-volatility, which imploded dramatically last Monday when VIX, also known as Wall Street’s fear gauge, registered its largest percentage change in its history, cratering bets that volatility measures would fall, if not remain muted.

Short volatility products, notably, VelocityShares Daily Inverse VIX Short Term ETN XIV, +11.89% tumbled 90% in after-hours trade Feb. 5 as the Dow Jones Industrial Averaged DJIA, +1.03% plunged 1,175 points, or 4.6%, marking its sharpest point drop in the blue-chip gauge’s 121-year history. Another product, the exchange-traded fund ProShares Short VIX Short-Term Futures ETF SVXY, +12.05% known by its ticker SVXY, also tanked last week.

Credit Suisse, the sponsor, of VelocityShares Daily, or XIV, said it planned to liquidate the product on Feb. 21.

The spectacularly wrongway short bets had become one of the most popular trades on Wall Street because volatility had gone eerily absent for a protracted period, encouraging investors, who were lamenting the narrow trading ranges present during that period of placidity, to make more aggressive wagers to generate richer returns. Those moves also came amid ultralow rates for government bonds, particularly the 10-year Treasury note TMUBMUSD10Y, +0.60%

Jason Zuckerman, attorney at law firm, Zuckerman Law, who is representing the anonymous whistleblower, told MarketWatch that his client is concerned about unfair markets.

“My client is concerned about VIX manipulation that has already caused investors to incur massive losses and is eager to prevent further harm from investors,” Zuckerman said.

The whistleblower would also like the market regulates to play a more active role in preventing further harm to investors including requiring more accurate and comprehensive disclosures about the various risks that are associated with products linked to VIX,” he said.

The letter urges “the SEC and CFTC to promptly investigate the matter before investors suffer additional losses due to this fraud.”

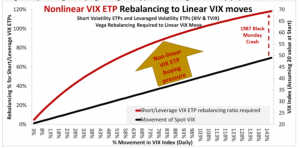

Zuckerman’s whistleblower further charges that the average retail investor isn’t aware of how exchange-traded products like XIV are rebalanced daily and that a “mismatch” in the nature of short-volatility products means “a larger move in spot-volatility in either direction requires excessive buying or selling pressure whenever short volatility assets are dominant.”

Source: Zuckerman Law

One error that market participants have pointed out is that Zuckerman and his client in the letter refer to the CME Group Inc., at one point rather than the Cboe Global Markets Inc., which oversees the VIX product.

“This letter is replete with inaccurate statements, misconceptions and factual errors, including a fundamental misunderstanding of the relationship between the VIX Index, VIX futures and volatility exchange traded products, among other things,” a Cboe spokeswoman said in a statement.

Messages to the SEC and the CFTC weren’t immediately returned.

The whistleblower claim also comes amid heightened regulatory scrutiny around short-VIX products, including former CFTC Commissioner Bart Chilton, who told MarketWatch that warnings about products like XIV should be written in “big, bold 24-point font and in red letters.”

A Cboe news release said that Feb. 5-Feb. 9 was the busiest week in the exchange’s history with a record weekly high of 48.29 million contracts traded. However, shares of Cboe, which merged with merged with Bats Global Markets last year, lost 20% last week when after the market mayhem cast doubt on whether these products would remain viable choices for traders.

Cboe executives are confident its VIX product will continue to do well in all market conditions. On its earnings call, John Deters, Cboe’s chief strategy officer, told analysts, “It’s really an exceptional event when the level of VIX increases and doubles in a matter of just a handful of days. That’s occurred, and now we’re at a point where — and professionals know this — we’re at a point where the short VIX strategy tends to work quite well.”

Cboe Chairman and CEO Edward Tilly refuted concerns about the impact of the problems at some exchange-traded products and added that the exchange saw record trading volume in VIX futures and options in 2017. “The activity we see from issuers of XIV and SVXY is less than 5% of all VIX futures trading, representing average daily volume of about 12,000 contracts,” Trilly said. Non-institutional holders of these ETPs were approximately 21% of total holdings in the last reported period, he said, with the remainder consisting of “sophisticated institutional users who employ inverse VIX ETPs as part of a diverse mix of trading and investing strategies.”